The Expiry Day Trap: Inside Jane Street’s Alleged $4 Billion Manipulation of India’s Options Market

Fifteen expiry days. One playbook. Roughly four billion dollars — allegedly extracted from the world’s largest options market before any regulator noticed how it was being done.

I. The Perfect Trade

On the morning of a BANKNIFTY expiry day, trading would begin. Index constituent stocks — Kotak Bank, Axis Bank, State Bank of India — would start moving above their last traded price. Not in one stock. Not erratically. In the key BANKNIFTY components, consistently, aggressively, and in volumes large enough to represent fifteen to twenty-five percent of the entire market-wide traded value in those securities within the opening session.

The index would rise. Sometimes by one percent. Sometimes by nearly one and a half. Retail traders watching their terminals would see green. Options desks would adjust their hedges. The market would seem, in the language of trading floors everywhere, to be finding support.

It was finding a trap.

In July 2025, India’s Securities and Exchange Board issued a 105-page interim order alleging that Jane Street Group — one of the most profitable trading firms on earth, generating $20.5 billion in annual revenue — had run this trap across fifteen of eighteen analyzed BANKNIFTY expiry days between January 2023 and May 2025. Alleged options profits across those fifteen sessions: ₹3,914 crore (~$470 million). Total unlawful gains over the full investigation period: approximately ₹32,681 crore — roughly four billion US dollars. SEBI responded by freezing ₹4,843.57 crore (~$566 million) in Jane Street assets and banning its entities from India’s securities markets entirely.

II. The Firm Nobody Talks About

Jane Street Capital was founded in 2000 by four former Susquehanna International traders working out of New York. It does not manage client money. It does not appear in the headlines alongside Goldman Sachs or Citadel. Until recently, most people outside quantitative finance had never heard of it. That obscurity is, by design, an advantage.

What Jane Street does — with exceptional proficiency — is arbitrage. The firm exploits pricing discrepancies between related financial instruments: between an ETF and its underlying basket, between futures and the spot market, between options and their theoretical fair value. Algorithms execute these trades at machine speed across correlated markets simultaneously. By 2024, the firm employed over 3,000 people across five offices in New York, London, Hong Kong, Amsterdam, and Singapore, trading stocks in 45 countries. It entered India officially in 2020, establishing local subsidiaries specifically to access the subcontinent’s derivatives markets.

India, it would turn out, was a very particular kind of opportunity.

III. The World’s Largest Options Casino

By traded volume, India is the world’s biggest equity derivatives market. That is not a marginal distinction. India’s derivatives turnover runs at over three hundred times the value of its cash equity markets. Weekly BANKNIFTY options — contracts on the Bank Nifty index settled every Thursday — attract tens of millions of retail traders, many of them speculating on short-term directional moves with contracts that expire within the same day or within days.

This creates structural inefficiencies. When millions of small participants buy weekly options without professional hedging frameworks, there is a persistent imbalance in how those options are priced relative to theoretical fair value. Large, well-capitalized firms with advanced algorithms can identify these imbalances and — in principle — profit legitimately. That is the industry’s standard defense of high-frequency trading: we provide liquidity, tighten spreads, make markets more efficient.

SEBI’s case is an argument that what happened in India did not discover market inefficiencies. It manufactured them — and then collected from the people on the other side.

How Index Options Work

BANKNIFTY options are contracts that give the buyer the right — not obligation — to buy or sell the index at a fixed price on expiry day. Sellers collect a premium upfront. If the index moves against the buyer, the contract expires worthless. The options market is zero-sum: every rupee of buyer loss is a rupee of seller profit.

On expiry Thursdays, open interest is at its peak. Price moves in the final hours can cause massive, rapid shifts in option value — making expiry day the most lucrative and the most manipulable session of the month.

IV. The Scheme: Fifteen Days, One Playbook

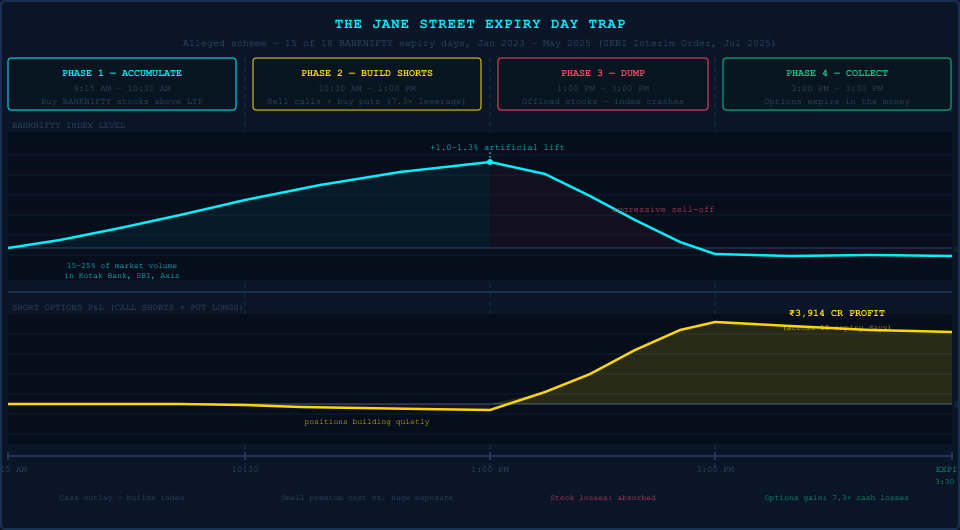

SEBI’s interim order reconstructs the alleged method in granular detail, drawing on order flow data and the timing relationships between Jane Street’s cash market activity and its derivatives positions. The pattern repeated across fifteen expiry days with a consistency that SEBI argued was statistically impossible to attribute to routine hedging. Three phases defined each session.

Phase 1 — Building the Pressure (9:15 AM to ~10:30 AM)

In the opening session, Jane Street entities began purchasing large quantities of BANKNIFTY constituent stocks and index futures. Orders were placed above the last traded price — a technique that guarantees execution but, by definition, pushes prices upward with each fill. In the windows SEBI analyzed, Jane Street’s buying represented fifteen to twenty-five percent of the total market-wide trading volume in target stocks: Kotak Bank, SBI, and Axis Bank.

The aggregate effect on the Bank Nifty index was measurable: an artificial elevation of 1% to 1.3%, according to SEBI’s analysis. On a multi-trillion-rupee benchmark, that is not noise. It is enough to materially shift the settlement calculus of every outstanding options contract referencing that index — pushing out-of-the-money call options toward the money, pushing in-the-money puts further in.

The cash market buying was not designed to profit from stocks going up. It was designed to move a benchmark to a temporarily elevated level and hold it there long enough for what came next.

Phase 2 — The Invisible Short (Concurrent, escalating through midday)

Simultaneously — not after, but during — Jane Street was building positions in the derivatives market positioned to profit if the index fell. Selling call options. Buying put options. The net derivatives exposure was a large, leveraged short on the same index that Jane Street’s stock purchases were artificially inflating.

SEBI documented the scale of this leverage precisely. The ratio between Jane Street’s options exposure and its equivalent stock market exposure: 7.3 to 1. For every rupee of upward price pressure applied through cash market purchases, the corresponding notional derivatives position was seven times larger — and pointed in the opposite direction.

The counterparties on the other side of those options trades were, predominantly, retail participants who saw an index rising and drew the rational inference that momentum favored the upside. They were buying calls and selling puts into the hands of an entity that had manufactured the conditions creating that inference. The mispricing was not found. It was built — and then sold.

Phase 3 — Springing It (1:00 PM to ~3:00 PM)

In the afternoon session, the reversal. Jane Street entities offloaded the stocks and futures accumulated in the morning, selling aggressively. The mechanism that had lifted the index in the morning now ran in reverse. Sell orders drove constituent stock prices down. The Bank Nifty index fell. On expiry days, when options contracts settle against the closing index value, the direction of that late-session move determines whether positions expire profitable or worthless.

SEBI also identified a secondary variant used on three of the eighteen analyzed days: “marking the close” — large sell orders entered specifically in the final minutes of trading to skew the settlement price downward. More surgical than the standard reversal. Targeted directly at the expiry settlement mechanism rather than the broader session.

The cash market losses from selling stocks below purchase price were real. But they were dwarfed by the options gains — by the documented 7.3 factor. Losing one rupee in the cash market to gain seven in derivatives is not a trading error. SEBI argues it is the business model.

The Score

Across fifteen BANKNIFTY expiry days: ₹3,914 crore (~$470M) in index options profits. Over the full January 2023 to May 2025 investigation period: approximately ₹32,681 crore (~$4 billion) in alleged unlawful gains. Cash market losses used to manufacture the moves: substantial, but a fraction of the derivatives take. That ratio — 7.3 to 1 — is the signature of the scheme in the data.

SEBI’s Key Findings at a Glance

- 15 expiry Thursdays targeted between January and October 2023

- ~$4 billion in alleged profits across the trading period

- $566 million in assets frozen — Jane Street’s Indian accounts impounded

- 105-page order documenting the alleged three-phase playbook in detail

- Jane Street barred from India’s securities markets pending final adjudication

V. How a New York Lawsuit Unravelled Everything

SEBI’s investigation did not begin in Mumbai. It began in a Manhattan courtroom.

In April 2024, Jane Street filed suit in the Southern District of New York against Millennium Management for allegedly poaching two traders — Doug Schadewald and Daniel Spottiswood — who had worked directly on Jane Street’s India options strategy before departing to a competitor in 2023. In the filings, Jane Street described this strategy as generating over one billion dollars in profit in 2023 alone. The firm argued the methodology constituted a protectable trade secret.

The filings were public. SEBI read them. What had been an entirely internal operation — one Jane Street considered valuable enough to pursue nine-figure litigation to defend — was now a documented, quantified, publicly accessible description of a market-moving strategy operating across Indian derivatives markets. The regulator opened a formal investigation. By February 2025, the NSE had issued an explicit advisory to Jane Street regarding its trading practices. By July 3, 2025, the 105-page interim order had landed.

The Millennium case settled on December 5, 2024, on undisclosed terms. The damage, from Jane Street’s perspective, had already been done. The outline of its India strategy was in the public record — and in the hands of the one regulator in a position to do something about it.

VI. The Response: $566 Million Frozen

SEBI’s interim order froze ₹4,843.57 crore in assets held across four Jane Street entities: JSI Investments Private Limited, JSI2 Investments Private Limited, Jane Street Singapore Pte Ltd, and Jane Street Asia Trading Limited. Banks holding those assets were instructed to permit no debits without explicit SEBI authorization.

Eleven days after the order, on July 14, 2025, Jane Street deposited the full frozen amount into escrow, reserving its right to appeal. In September 2025, the firm filed an appeal with India’s Securities Appellate Tribunal. As of March 2026, the SAT hearing has been adjourned pending full proceedings. No final adjudication has been issued.

Jane Street’s defense rests on two arguments. The substantive one: the trades constituted legitimate index arbitrage — standard practice in which derivatives exposure is hedged by trading underlying securities. The procedural one: the NSE’s own surveillance department initially found no evidence of manipulation in the majority of analyzed sessions, and a later inter-departmental review reaching contradictory conclusions was not disclosed to Jane Street during the investigation. The firm also claims it was denied access to key NSE-SEBI correspondence material to its defense.

Whether either argument prevails is a matter for the SAT. What is established — in the deposited escrow, in the regulatory filings, in the court record of the Millennium case — is a factual foundation that survives the ongoing appeal.

VII. A Pattern Across Borders

The India case is the largest and most detailed regulatory action involving Jane Street. It is not the only one.

The Terraform Connection — New York, 2026

On February 23, 2026, Todd Snyder — the bankruptcy administrator overseeing the remnants of Terraform Labs, whose UST algorithmic stablecoin collapsed in May 2022 and destroyed approximately forty billion dollars in value — filed suit against Jane Street Group in the Southern District of New York (Case 1:26-cv-1504). Named defendants include Jane Street co-founder Robert Granieri and employees Bryce Pratt and Michael Huang.

The allegation is insider trading on non-public information about the UST depeg. The complaint contends that Bryce Pratt — a former Terraform intern subsequently hired by Jane Street — maintained back-channel communications with former Terraform colleagues that provided advance access to material non-public information. On May 7, 2022, Terraform quietly withdrew 150 million TerraUSD from the Curve Finance 3pool liquidity pool. According to the complaint, within ten minutes — before any public announcement — a wallet linked to Jane Street withdrew 85 million TerraUSD from the same pool. The timing, Snyder’s legal team argues, does not reflect coincidence.

Jane Street has denied the allegations, describing the suit as “a transparent attempt to extract money” and arguing that Terraform’s collapse was the product of its own management’s fraud and the inherent design flaws of the UST mechanism. The case is in early proceedings.

The Settled Trade Secrets Case — US, 2024

The Millennium trade secrets lawsuit, filed April 2024 and settled December 5, 2024, is notable for what it reveals about how seriously Jane Street regarded its India operation. A firm does not allege billion-dollar trade secret theft unless it believes the stolen information is genuinely worth that amount. The settlement terms were sealed. What was not sealed — what could not be unsealed — was the description of the strategy that the litigation made public, and which became the foundation of the SEBI investigation that followed.

VIII. Where Arbitrage Ends

Jane Street’s defense reflects a genuine tension in modern markets. High-frequency and quantitative trading firms do provide real economic value: tighter spreads, faster price discovery, more liquid markets. The distinction between exploiting a pricing inefficiency and creating one is not always visible from outside a trading system. Regulators in multiple jurisdictions have spent years trying to draw it.

What makes the India case structurally different from routine arbitrage allegations is scale. When a single firm represents fifteen to twenty-five percent of daily trading volume in specific stocks on a given day, it is not responding to market prices. It is setting them. At that gravitational weight, the arbitrage defense becomes difficult to sustain on its own terms: you are not discovering a mispricing and trading it to zero. You are creating a mispricing, extracting from it at leverage, and exiting before the correction lands on the counterparties who could not see the other side of the trade.

Whether courts and tribunals ultimately agree is unresolved. What is not unresolved is the documented record: a 105-page interim order, a $566 million escrow deposit, a co-founder named in a federal insider trading suit, and a trade secrets settlement that inadvertently handed investigators the roadmap. The question of whether sophisticated algorithmic trading constitutes arbitrage or predation has stopped being theoretical. It is now being argued by lawyers in Mumbai and Manhattan simultaneously.

IX. When the Market Itself Is the Target

The Jane Street case operates at the scale of a national benchmark index — manipulation through the sheer gravitational mass of capital. But the underlying logic appears wherever a party occupies a position of structural advantage over other market participants. GRIDNET’s own market on XT.com encountered a smaller-scale variant in 2025: systematic front-running, sandwich attacks, and order sniping that exploited the exchange’s own market-making rules, achieving — according to technical analysis — “100% snipe accuracy with zero misses” on randomized orders, a result impossible without advance knowledge of the order flow. The full technical post-mortem is documented by the development team at the GRIDNET dev forum.

In neither case did manipulation require breaching a system. It required only occupying the right position within one — and being willing to use the advantage it conferred.

Markets function because participants assume the price on their screen reflects collective reality rather than the output of someone else’s strategy. The moment that assumption breaks — at any scale, in any jurisdiction — the exchange of value becomes the extraction of it. What SEBI documented across fifteen expiry days in India is, if the allegations are sustained, not a technical violation of a trading rule. It is a systematic answer to a question most retail participants never thought to ask: who is on the other side, and what do they know that we don’t.

References & Sources

- SEBI — Interim Order in the Matter of Index Manipulation by Jane Street Group, July 3, 2025. Official SEBI Order (sebi.gov.in)

- CNBC — “Indian Regulator Bars US Trading Firm Jane Street from Accessing Securities Market,” July 4, 2025. CNBC

- Bloomberg — “Jane Street, Millennium Settle India Options Trade Secrets Case,” December 5, 2024. Bloomberg

- Bloomberg — “Jane Street Sued for Insider Trading by Terraform Administrator,” February 24, 2026. Bloomberg

- NPR — “How Jane Street Made $4 Billion from India,” September 24, 2025. NPR

- Oxford Law Blogs (OBLB) — “Jane Street and the Expiry Day Trap: Unpacking SEBI’s Crackdown on Algorithmic Trading,” 2025. Oxford OBLB

- Business Standard — “Jane Street Files Case Against SEBI’s Market Manipulation Charge,” September 3, 2025. Business Standard

- CoinDesk — “Jane Street Faces Claims of Insider Trading that Sped Up Terraform’s 2022 Collapse,” February 24, 2026. CoinDesk

- Bloomberg — “India Gets Tough on High-Frequency Trading with Jane Street Crackdown,” July 6, 2025. Bloomberg

- FTI Consulting — “When Algorithmic Trading Meets Allegations of Market Manipulation,” 2025. FTI Consulting

- GRIDNET Development Team — “EPIC 1.9.5 Release Notes: XT.com Feedback from Dev Team,” 2025. GRIDNET Dev Forum