From XT.com’s Black Box to

Hyperliquid’s Glass House

A Builder’s Journey

How centralized exchanges weaponize market making rules to extract wealth from their own listed projects — and why we are building a bridge to Hyperliquid, the transparent alternative.

The Illusion of Liquidity

Every founder who has listed a token on a centralized exchange knows the ritual. You pay the listing fee — $40,000 USDT is standard for mid-tier exchanges. You deposit your market-making bags as required. You integrate their API, build your trading bots, optimize your order placement. You do everything right.

And then, within seconds of going live, you watch the entire market depth explode across the full spectrum — buy orders and sell orders materializing at 50x the current price, as if thousands of eager traders had been waiting for this exact moment. All within 1 to 3 seconds.

That should have been the first warning.

The crypto industry has normalized something that would be a federal crime in traditional finance: exchanges trading against their own customers. Not through sophisticated market-neutral strategies. Not through legitimate arbitrage. Through raw, unrestrained front-running — a Python script that sits above the order book, extracting value from every single trade you make, with zero timing constraints and zero accountability.

This is not a hypothetical. This is our story.

The Market Making Trap

Centralized exchanges don’t just charge you a listing fee. They require you to provide liquidity — to maintain a certain spread, to keep order books looking active, to create the impression that the exchange has real traders. This is euphemistically called “market making requirements.”

In practice, here is what those requirements look like:

- You must maintain buy and sell orders within a specified price gap at all times.

- You must deposit significant bags of your own token as collateral.

- You must perform wash trading — executing trades against yourself to maintain “volume.”

- You must keep your market-making bot running 24/7 or face delisting threats.

Every exchange requires this. It has become the norm. And the reason is simple: without projects artificially inflating their own trading volumes, most CEX trading pairs would show what they truly are — ghost towns with zero organic activity.

But here is where it gets predatory. The exchange knows exactly when and how you place your market-making orders. They see your API calls before they hit the order book. They know your patterns, your timing, your constraints. And they use that knowledge to extract maximum value from you.

|

$40K+

Typical CEX listing fee (USDT)

|

$1K/day

Losses to front-running (our experience)

|

|

95%+

Estimated fake volume on many CEX pairs

|

798 HYPE

Hyperliquid listing (Dutch Auction)

|

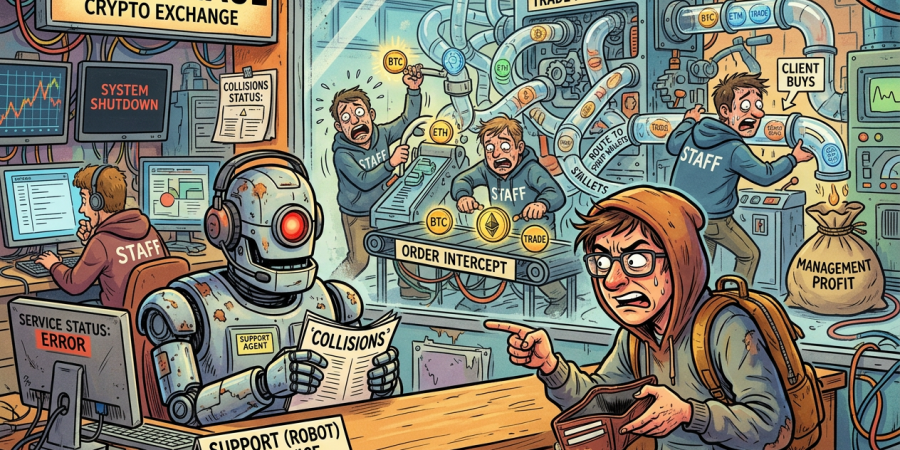

Front-Running From the Inside: Our Experience With XT.com

We listed GNC on XT.com. We did everything by the book. Years of work went into it — stability improvements, network hardening, API integration. The listing itself was a milestone. XT.com’s interface looked professional: TradingView charts, a polished mobile app, clean design. We were genuinely optimistic.

The end result? XT.com never had to update GRIDNET Core manually. It never crashed on them. Not a single support ticket. Not a single operational issue. The technology was bulletproof.

But then we started watching the charts.

Phase 1: The “Arbitragers”

Within seconds of listing — literally 2 to 3 seconds — the entire market depth appeared across both sides. Buy orders and sell orders materialized across the full price spectrum as if an army of traders had been waiting. The speed alone should have told us everything. No human traders operate that fast. No legitimate arbitrage bot deploys across the full depth spectrum simultaneously.

We noticed constant high-frequency price fluctuations from day one. The pattern was mechanical, relentless, and consistent:

- They buy when the market is thin.

- We deploy market-making sell offers — as required by their rules, with bags as required by their rules.

- The moment we do, they sell.

The cycle repeated endlessly. Buy low when we had no sell wall up. Wait for us to place our required market-making orders. Dump into our liquidity. Extract USDT. Repeat.

When we raised concerns, XT.com had a ready explanation: “There are some arbitragers placing small orders. These small orders are causing COLLISIONS in our system.”

Collisions. Their word. Nobody here will forget it.

Phase 2: The API Lock Illusion

XT.com offers a feature where only the designated market maker can access a trading pair via API. Once enabled, no third-party bot should be able to trade GNC/USDT through the API. It was enabled by default for us.

We thought this was wonderful. A competitive advantage. No external bots could front-run our orders, right?

Wrong. Catastrophically wrong.

Despite being the only account with API access, our orders were being filled within milliseconds. Not seconds. Milliseconds. We spent days and weeks optimizing high-frequency order placement in Python — adjusting thread priorities at the operating system level, minimizing network latency, ensuring our orders executed at the absolute fastest possible speed.

No luck. The fills were instantaneous. Whatever was filling our orders existed inside the exchange’s matching engine, operating before orders even reached the order book.

When confronted, XT.com maintained their position: “These are legitimate trading operations from third-party traders causing collisions. Such activities cannot be prevented.”

We were reportedly the only ones with API access to the GNC/USDT pair. Let that sink in.

Phase 3: The Batch Order Proof

We decided to eliminate all possible explanations. We switched to batch API orders — placing a BUY and a SELL as part of a single API call. This is an atomic operation. Both orders should hit the order book simultaneously. There should be no window for any third party to intervene.

The buy limit order was getting filled. The sell limit order was not. Someone else was filling our buy — even within an atomic batch call.

At that point, we knew. There is no mechanism in this universe by which an external party could front-run the internals of a batch API call. The only entity capable of intercepting and selectively filling orders within a single API call is the exchange itself.

Phase 4: Every Countermeasure Defeated

We tried everything:

- Zero-spread orders: We placed buy orders right below the best sell offer, eliminating the spread entirely so there would be no room for a better buy offer. It worked for 2-3 days. Then it didn’t.

- Post-only flags: We used order flags that reject a limit order if it would instantly execute (meaning if a matching order already exists). This should have prevented our orders from dumping into their hidden orders. Worked for 2-3 days. Then it didn’t.

- High-frequency show/hide: We invited colleagues with decades of high-frequency trading experience. We built systems that showed and hid orders at both sides of the market at high frequency. There were moments when everything operated fine for minutes, sometimes hours. Then — instant fills, instant buys, as if a script had been watching and waiting.

- Sell-first wash trading: We tried placing sell limit orders first instead of buy orders. They would front-run that too — placing a better sell limit order at a slightly lower price, or at the same price (FIFO order books execute earlier orders first, and theirs was always earlier).

Their front-running systems were not just sophisticated. They were exhaustive. Every strategy we deployed was countered within days, sometimes hours. The system adapted. It learned our patterns. It extracted maximum value regardless of approach.

The Financial Toll

If we’d known their hostile “tax” would cost around $1,000 per month, we might have tolerated it. But they were far more predatory than that. $1,000 could be drained from our market-making accounts in a single day — easily. With every “high-frequency security” measure we implemented, every optimization we built. The USDT was being extracted as if there was no tomorrow.

The only “solution” would have been to keep placing sell orders of GNC relentlessly, destroying our own tokenomics as they kept buying at artificially depressed prices. That is not a solution. That is capitulation.

The Fundamental Problem

Here is what finally crystallized for us: if the exchange itself is pumping and dumping your token — if the entity operating the trading floor is the one manipulating the price — then the chart itself might be completely fake. How would you know? You cannot audit their order-matching engine. You cannot verify that the price you see reflects actual supply and demand. You are operating inside someone else’s black box, and they hold all the keys.

It took us 2 to 3 months to become 101% confident that this was happening. Two to three months of burning development time investigating low-level trading mechanics instead of building the technology we should have been building. That is the true cost — not just the USDT, but the engineering hours, the morale, the distraction from our mission.

The Structural Problem With Centralized Exchanges

Our experience with XT.com is not unique. It is a symptom of a structural problem that plagues the entire centralized exchange industry. When the entity that operates the trading floor also has the ability to trade on the trading floor — with privileged access to order flow, latency advantages measured in microseconds, and zero external oversight — predatory behavior is not a bug. It is an inevitability.

Consider what a centralized exchange actually is: a private company that controls the order book, the matching engine, the user balances, and the reported trading volume. They can:

- Fabricate volume. Most trading volume on CEXes is fake. Studies have consistently estimated that 70-95% of reported volume on many exchanges is wash trading, manufactured either by the exchange itself or by projects forced to do it to meet listing requirements.

- Manipulate price. If you control the matching engine, you control the price. You can front-run, back-run, sandwich attack, or simply manufacture the order book state that produces your desired outcome.

- Hold assets hostage. Your tokens are in their wallets. Withdrawal delays, “maintenance” windows, surprise delistings — all of these are leverage the exchange holds over every listed project.

- Extract rent through market-making requirements. By requiring projects to maintain liquidity (read: provide a steady supply of USDT for the exchange to siphon), they create a permanent extraction mechanism disguised as a service requirement.

Which project would prefer to put their hard-earned money into a CEX black box, having no way to know if the chart is even real?

As Time Approaches Infinity: The CEX Obsolescence Thesis

Here is our thesis: as time approaches infinity, there will be little to no incentive for traders to use centralized exchanges.

This is not wishful thinking. It is a consequence of technological convergence. Every year, decentralized exchange technology becomes faster, cheaper, and more capable. Every year, the gap between what a DEX can offer and what a CEX claims to offer narrows. And every year, another exchange gets hacked, another founder discovers they’ve been front-run, another project loses its listing with no recourse.

The transition is accelerating because of a fundamental asymmetry: decentralized exchanges can only get better, while centralized exchanges cannot fix their core architectural flaw — they require trust in an opaque intermediary, and that trust is increasingly unjustifiable.

In the past, decentralized exchanges were the domain of tokens deployed atop Layer 1 projects — ERC-20s on Uniswap, SPL tokens on Raydium. We propose this model be extended further, toward coins and tokens of any kind — including native Layer 1 coins from independent blockchains like GRIDNET OS. Awareness across the decentralized community needs to increase. It has been far too long that CEXes have required artificial market making, artificial pumping of price action from project owners. In fact, such demands have become a requirement — a cost of doing business — creating an elaborate illusion that the exchange has legitimate trading activity.

Hyperliquid: The Transparent Alternative

Hyperliquid is a purpose-built Layer 1 blockchain with an on-chain order book. Not an AMM. Not a liquidity pool. An actual order book — the same structure used by the New York Stock Exchange, the London Stock Exchange, and every serious trading venue in the world — except fully transparent and on-chain.

On Hyperliquid:

- Everyone sees by whom and with whom orders are matched. Every trade, every fill, every address — verifiable on-chain.

- When someone does wash trading, everyone sees it. You can see between which addresses volume is flowing. You can tell when volume is real and when it is fake. A dream come true.

- No one can delist you. Once a spot ticker is purchased via Dutch auction, it stays forever. Validators vote only on perpetual delistings — spot tokens are permanent.

- No market-making requirements. No enforced wash trading. No price gap mitigations. No monthly fees for “liquidity support.” None of it.

- No artificial price action demands. You are not required to pump your own token. You are not required to maintain the illusion of activity. If your token has real demand, the chart shows it. If it doesn’t, the chart shows that too. Honesty.

While this does not create easy price manipulation and artificial price action — that is precisely what a proper, honest technology needs. A proper project requires a proper exchange service. Simple as that. We believe Hyperliquid delivers exactly that.

GRIDNET OS x Hyperliquid: A First-of-Its-Kind Integration

GRIDNET OS is a Layer 1 blockchain with its own decentralized state machine, its own proof-of-work consensus, its own scripting language (GridScript), and its own virtual machine. It is not an ERC-20 token deployed on Ethereum. It is not a Solana program. It is an independent, sovereign blockchain.

This makes bridging to external chains a fundamentally different challenge than what most DeFi projects face. We are not calling a smart contract on the same chain. We are connecting two completely independent blockchain architectures — GRIDNET OS with its UTXO-based transaction model and Ed25519 cryptography, and the Ethereum-compatible ecosystem powering Arbitrum, LayerZero, HyperEVM, and HyperCore.

We believe we are the very first Layer 1 project with less than $1 billion total valuation to attempt cross-chain integration with Hyperliquid. We never follow easy paths. We strive to push the boundaries of decentralized technology, and this bridge represents one of the most ambitious cross-chain integrations attempted by an independent blockchain project.

Even though for a project such as ours — a Layer 1 with its own decentralized state machine — integrating with external blockchains is a very extensive endeavor, we find this journey worth taking. In the end, we spent over $300,000 USDT on the Liquidius Maximus sub-project (our comprehensive market making and bridge infrastructure). We always strive to have our hearts full of humility — but we believe the Liquidius Maximus suite is a work of art.

The Bridge Architecture

Our Bridge Coordinator service connects GRIDNET OS to the Hyperliquid ecosystem through a sophisticated multi-path architecture. We integrate with four distinct blockchain environments: Arbitrum (as the EVM settlement layer), LayerZero (for cross-chain messaging), HyperEVM (Hyperliquid’s EVM-compatible layer), and HyperCore (Hyperliquid’s native high-performance trading engine).

The architecture uses a hybrid Lock/Unlock + Mint/Burn model — battle-tested at scale (WBTC operates at $10B+ using this pattern). On the GRIDNET side, native GNC is locked in a reserve address. On the Arbitrum side, wrapped GNC (wGNC) is minted or burned as needed. LayerZero’s OFT (Omnichain Fungible Token) standard handles the cross-chain messaging between Arbitrum and HyperEVM.

Five Paths, One Bridge

We have successfully evaluated all five bridging paths connecting GRIDNET OS to the Hyperliquid ecosystem on testnet. Our architecture provides a balance between high-speed liquidity and trustless fallbacks.

Outbound: GRIDNET OS to Hyperliquid

Path A: The Canonical OFT Path

Route: GRIDNET OS -> Arbitrum (mintWithId) -> OFT Adapter -> LayerZero -> HyperEVM

GNC arrives as an ERC-20 OFT in your HyperEVM wallet. This is the fully decentralized canonical path — no coordinator reserve required. 6 hops, approximately 15 to 45 minutes latency depending on DVN relay speed.

Path B: The Spot Composer Path

Route: Path A + HyperLiquidComposer contract on HyperEVM

Extends Path A by automatically converting the OFT token into a native HyperCore spot balance via the Composer precompile. 7 hops, approximately 30 to 45 minutes. The result lands directly in the user’s HyperCore trading account.

Path C: The Outbound Fast Lane (R7)

Route: GRIDNET OS -> Coordinator Monitoring -> Direct spotSend from Coordinator Reserve

The performance path. The coordinator detects the user’s GRIDNET bridge transaction and immediately executes a HyperCore CoreWriter spotSend from its own reserve. GNC lands in the user’s HyperCore spot balance in 2 to 5 minutes with only 4 hops. Bypasses Arbitrum and LayerZero entirely. Falls back to Path B automatically if the coordinator reserve runs low.

Inbound: Hyperliquid to GRIDNET OS

Path D: The Inbound Canonical Path

Route: HyperEVM OFT Send -> LayerZero -> Arbitrum BridgeBurn -> GRIDNET unlock

The fully decentralized return path. 7 hops, approximately 30 to 45 minutes. GNC is burned on the EVM side and unlocked from the GRIDNET reserve.

Path E: The Inbound Fast Lane (R8)

Route: User spotSend to Coordinator address (with GRIDNET destination in memo) -> Direct GRIDNET unlock

The symmetric high-speed return path. Users send GNC to the coordinator’s HyperCore address with their GRIDNET destination in the memo field. The coordinator detects the fill, validates the intent, and unlocks GNC directly on GRIDNET. 4 hops, 2 to 5 minutes.

Security Through Formal Verification

This is not a move-fast-and-break-things bridge. We have subjected every path, every state transition, and every edge case to rigorous formal verification and adversarial auditing.

TLA+ Formal Specification

The entire bridge state machine is modeled in TLA+ (Temporal Logic of Actions) — the same formal specification language used by Amazon Web Services to verify their distributed systems. Our specification currently contains 40 safety invariants verified by the TLC model checker across over 25 million explored states with zero violations.

Key invariants include:

- Solvency: The GRIDNET reserve balance must always be greater than or equal to the total wGNC in circulation across all chains.

- No double-spend: Every bridge transfer can only be processed once. Atomic intent claiming prevents race conditions between concurrent fills.

- No orphaned assets: Every locked GNC on GRIDNET has a corresponding minted wGNC, and vice versa.

- Fork safety: GRIDNET PoW fork detection with configurable key-block grace periods ensures transactions are only finalized after sufficient proof-of-work accumulation.

Adversarial Security Audits

We have completed 16 rounds of security auditing, spanning smart contracts, coordinator logic, blockchain-native attack vectors, and concurrency analysis. The audit program has identified and fixed:

- 4 CRITICAL vulnerabilities — including bridge intent front-running (PT-01), R8 double-match race condition (BC-14), TLA+ model gap in retry paths (TLA-R15-01), and unmatched fill flooding (R15C-01).

- 15+ HIGH vulnerabilities — including nonce sequencing races, XSS in the dashboard, gas limit validation, OFT dust truncation, and crash-gap recovery across all routes.

- 30+ MEDIUM/LOW issues — covering metadata cleanup, cursor persistence, rate limiting, decimal precision, and reorg protection.

E2E Testnet Validation

All six primary routes have been verified active on testnet with 122 completed transfers out of 139 total (the 17 failures are all legacy transfers from before security fixes SC-01/02 were applied). Key validation results:

- R8 (HyperCore to GRIDNET Direct): 33 seconds end-to-end.

- R1 (Arbitrum to GRIDNET): 448 seconds with full BridgeBurn and GRIDNET unlock.

- R7 (GRIDNET to HyperCore Direct): Completed after coordinator restart — gap recovery handled it autonomously.

- BC-KB-01 (PoW grace period): Validated on all four GRIDNET-sourced routes — transactions are held in PENDING_KEYBLOCK until sufficient proof-of-work key-blocks have been produced.

The coordinator survived multiple unplanned restarts during testing. In every case, gap recovery mechanisms detected missed events across all four source networks and resumed processing autonomously. No manual intervention required. No assets lost.

The Road to Mainnet

How many projects are there who would not even have the firepower to investigate exchange manipulation to this extent? A global exchange with a polished app, TradingView charts, thousands of trading pairs — they must be legitimate, right?

Wrong.

We cannot imagine young founders saving massive amounts of money to get listed on a CEX — $40,000 USDT listing fee, plus market-making fees, plus mandatory deposits. That is a lot of money to many people. Freedom-oriented projects, raising money in their communities. Can’t even think of it.

After all, not only scientists deploy coins on exchanges. Some of these projects are built by people for whom $40,000 represents years of savings. The thought that their carefully accumulated capital is being systematically siphoned by the very platform they trusted — it fills us with rage. Pure rage.

So we are burning our hearts toward Hyperliquid. We are going to enter the trading floor ready for anything. We have been through many things and we are not stopping. Were it solely for money, we would have been creating meme coins on PancakeSwap long ago.

But that is not why we build. We build because the technology matters. Because decentralization is not a marketing slogan — it is a fundamental architectural choice that eliminates entire classes of predatory behavior. Because a transparent order book is not just technically superior — it is morally superior.

Once you buy a spot ticker on Hyperliquid, it stays forever. Nobody can delist you. No one requires market-making compliance. No hidden Python scripts front-running your orders before they touch the book. No “collisions.” No black boxes.

Wild wild west. And we feel good about it.

|

5

Verified bridging paths

|

40

TLA+ safety invariants

|

|

25M+

Model-checked states

|

122

Completed testnet transfers

|

A Call to the Decentralized Community

We are publishing this article not just to document our journey, but to issue a call to the broader decentralized community. If you are a Layer 1 project, a DeFi protocol, or an independent token — you do not have to accept the CEX status quo. Decentralized exchanges like Hyperliquid offer a real, working alternative. The technology is ready. The infrastructure exists. What remains is for projects to have the courage and technical capability to make the leap.

It has been far too long for centralized exchanges to demand artificial market making, to require projects to pump their own price action, to operate opaque order books that may or may not reflect reality. The norm should be transparency. The standard should be verifiability. The expectation should be that when you see a trade on the chart, it actually happened between two independent parties.

We are probably going to provide market-making services to third-party projects — not as a main source of income, but out of passion. The Liquidius Maximus suite was built through fire, and we believe other projects deserve access to tools forged in that same crucible.

The future belongs to transparent markets. We are building the bridge to get there.